By Duncan Hill, Marketing Director, Davies & Associates

Our clients have always been interested in the UK, but we have certainly seen a spike since President Trump suspended a whole lot of US visas in April (and then a whole lot more last week).

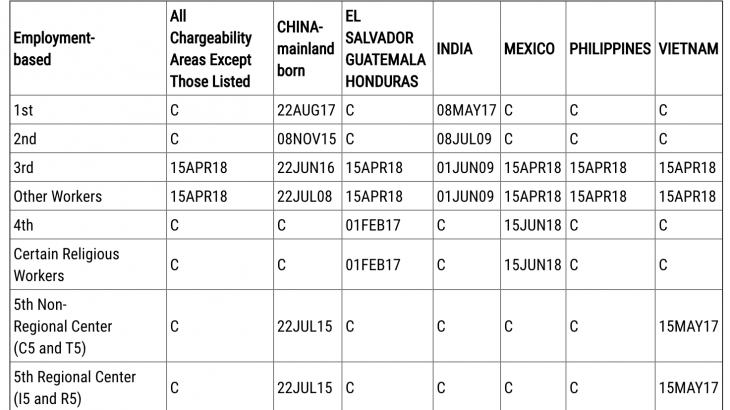

The first thing to say is that not all US visas have been suspended. We specialize in two key categories that are exempt. The EB-5 Immigrant Investor Visa Program and the E-2 Treaty Investor Visa were not included by President Trump, probably because they create jobs and promote investment in the United States.

Nevertheless, our teams around the world are noticing above-average-levels of interest in Britain, especially from clients and agents in Vietnam and India.

One of the ostensible aims of Brexit is to create a more “Global Britain“, attracting the best and brightest from around the world. As part of that, a new points-based immigration system will be introduced next year. Points will be awarded for things like English-language capability, salary bands, and education levels.

As the UK gears up to this, one change has already been made with the introduction of the Global Talent Visa in February. This change is rather more one of style than substance, since it is mostly a rebranding of the “Exceptional Talent Visa”

The Global Talent Visa is one of a range of so-called “Tier One” visas offered by the British government. Tier One visas are for “high-value migrants”, such as people bringing investment or talent. By contrast, Tier Two visas are for skilled immigrants with a job offer in the UK.

Another Tier One visa is the Investor Visa, which requires a minimum £2 million investment in UK bonds or shares. Anyone with this visa can apply for Indefinite Leave to Remain (IDLR) in the UK after five years. That waiting time can be reduced to three years for a £5 million investment or two years for a £3 million investment. It is possible to apply for UK citizenship 12 months after obtaining IDLR, subject to certain other requirements.

| Investment Amount | Apply for Indefinite Leave to Remain |

| > £2 million | 5 years |

| > 5 million | 3 years |

| > 10 million | 2 years |

The Innovator Visa and the Start-Up Visas, are also classified as Tier One. These visas are very similar in that they target people with a business idea that is deemed innovative, viable and scalable.

Where they differ is in the stage of development of the businesses they target. The Start-Up visa targets early stage companies and does not require any investment requirement, whereas the Innovator Visa targets slightly more mature firms by requiring minimum investment funds of £50,000.

Start-up visa holders are expected to transition to the Innovator visa when they can prove they have hit the funding threshold. After three years, anyone with an innovator visa can apply to settle in the UK, subject to certain other conditions.

All of these visas will be transitioned to the points based system in a favourable way. So, for example, a £2 million investment will give a person 75 points meaning they automatically exceed the 70-point-minimum threshold for entry.

While there is still considerable uncertainty surrounding immigration policy as the Brexit negotiations drag on, one thing is clear: The UK still wants to attract the “best and the brightest” to its shores.

Davies & Associates has offices in the United Kingdom and throughout the world. We are able to offer advice on the best ways for you to move your business and family overseas. As a law firm with both immigration lawyers and corporate lawyers, we are able to help our clients not just obtain visas, but to establish their firms overseas and stick by their side as they prosper.

Nothing in this blog constitutes legal advice. Please contact Davies & Associates to schedule a free consultation.